EMI × Kohler · Marketplace Intelligence

Kohler Thailand

Home & Living Marketplace Review

Lazada & Shopee · January–April 2026

An executive synthesis of category performance, Kohler's competitive position, brand differentiation and the outlook — built from EMI's monthly decks and SKU-level marketplace data. Every figure is click-to-source.

Executive Summary · Market Size · Kohler Share · Trends & Platform · Growth vs Market · Competitive Landscape · Differentiation · 6-Month Outlook · Action Plan · Sources

01 · Executive Summary

The six things to know

- Kohler is the #2 sanitaryware brand on Thai marketplaces. It holds ~20.5% of the tracked competitive set in April — up from #3 in January to #2 since February — and ~41% of all Official-store sales in the set. source

- Kohler is gaining share where it counts. +5.3 share-points within the branded set from January to April, even as direct premium rival American Standard collapsed (−82% sales, −14.8pp). source

- April's softness is seasonal, not structural. The whole category fell ~17% month-on-month in April after the Q1 peak, yet remains up ~136% year-on-year (moving annual total). source

- Channel control is best-in-class. 90% of Kohler's sales run through Official stores, vs Cotto 62% and American Standard just 7% — limiting grey-market leakage and protecting price integrity. source

- But Kohler is discount-dependent. A 48% average discount — the deepest in the set (rivals 12–29%) — and 91% of sales run on promotion, on a premium ฿2,253 ASP with 97% of sales above ฿700. Volume is being bought with price: the key margin and brand-equity risk. source

- Marketplace is only half the picture. External research (Aissistance Deep Research) flags two adjacent fronts that materially shape Kohler's Thailand strategy: a productised installation moat (Shopee/Lazada logistics are 1.4★; Thai consumer-forum evidence of disastrous third-party installs is endemic) and the B2B luxury-developer pipeline (Sansiri's 80% focus on ฿15M+ housing, AP Thailand's ฿55bn pipeline) where premium smart fixtures are now specification line-items, not consumer purchases. Outside this report's e-commerce remit, but they sharpen the action plan below.

02 · Market & Category Size

A ฿1.3bn category, heavily skewed to Shopee

Thailand's Home & Living category on Lazada + Shopee turned over roughly ฿1.3bn in Jan–Apr 2026 (~฿310–360M per month). Shopee is ~88% of it.

April category sales were ฿323M on our read of the raw listings — consistent with the EMI deck's reported ฿311M for April. An important caveat for interpretation: ~45–50% of this total is unbranded or generic merchandise (and some off-core items), so Kohler's competitive arena is the tracked sanitaryware brand set used throughout the rest of this report, not the headline category total. source: deck source: data

Category sales by month, split by marketplace (all listings). Derived from EMI × Kohler TH raw data, Jan–Apr 2026.

03 · Kohler Market Share & Position

#2 in the arena, and stronger among Official stores

Within the tracked sanitaryware set, Kohler rose from 15.2% (#3) in January to a 22–23% peak in Feb–Mar, settling at 20.5% (#2) in April behind market leader Cotto (~35% over the period). Among Official stores specifically, Kohler commands ~41% of the set — evidence of genuine brand pull rather than reseller-driven volume. source

Kohler share of the tracked sanitaryware competitive set, by month. Scope & method: see RECONCILIATION.md.

04 · Category Trends & Platform

Shopee is the battleground; Q1 peaks then cools

Shopee accounts for ~88% of category sales and an even larger share of the branded set (Apr: ฿23.7M Shopee vs ฿5.5M Lazada). The category's 13-month trajectory is firmly up year-on-year, with a pronounced Q1 high followed by an April pull-back — a seasonal rhythm rather than a downturn. source

Platform split by month, Jan–Apr 2026 (all listings).

The longer view — 13-month trend & seasonality

The EMI deck's 13-month rolling trend confirms the pattern: a Q1 build to a March peak, an April pull-back, and a category running well above last year. The April softness is the seasonal down-leg, not a reversal. (Click the source tag to view the EMI deck's 13-month trend slide.) source

05 · Kohler vs Market Growth

Outgrowing branded rivals; trailing the generic-fuelled category

Year-on-year, the category is up ~136% (MAT) and Kohler ~88% (฿95.6M vs ฿51.0M last year) — so Kohler grows slower than the total category, whose explosive growth is driven largely by generic and value listings. But against its actual competitors, Kohler is winning: it gained +5.3pp of branded-set share Jan–Apr while most rivals lost ground. source: deck source: data

Monthly sales indexed to January = 100, Kohler vs the competitive set. The April trough is shared across the set (seasonal).

06 · Competitive Landscape

Cotto leads, American Standard falters, value brands rise

Market leader Cotto (~35% of the set over Jan–Apr) still sits clear of the field but lost 3.1pp of set share over the period. The standout story is American Standard's collapse — −82% sales and −14.8pp share — vacating premium demand that Kohler is well placed to capture. Meanwhile value brands Karat Faucet, Moya and Karat all gained share, and small premium players (Hansgrohe, Toto, Jomoo) surged off low bases. source

Competitive-set ranking — Jan–Apr (cumulative)

| Brand | YTD sales (฿M) | YTD share | Δ share (Jan→Apr momentum) |

|---|---|---|---|

| Cotto | 64.7 | 35.3% | −3.1pp |

| Kohler | 36.1 | 19.7% | +5.3pp |

| American Standard | 25.7 | 14.0% | −14.8pp |

| Hafele | 21.8 | 11.9% | −2.1pp |

| Karat Faucet | 12.8 | 7.0% | +4.5pp |

| Moya | 11.2 | 6.1% | +3.6pp |

| Karat | 8.6 | 4.7% | +3.7pp |

| Toto | 1.3 | 0.7% | +1.2pp |

Tracked sanitaryware set, cumulative Jan–Apr 2026 (ranked by total period sales; the Δ column shows within-period momentum, e.g. American Standard's mid-period collapse). Full Top-10 brand detail by platform is in the deck. Shopee Top 10 Lazada Top 10

What's winning — and what it reveals

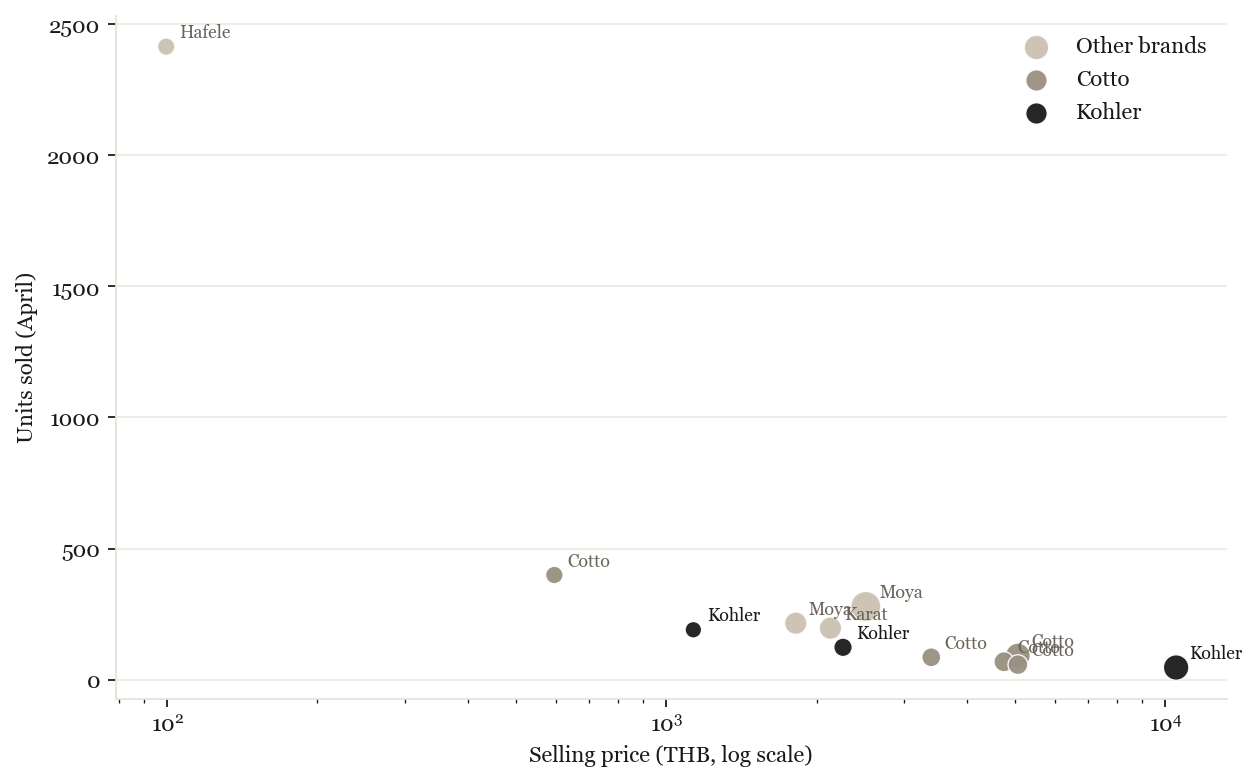

The bestseller list is a map of how each brand competes. Cotto owns it — 8 of the top 30 products, almost all toilets — sold across Official, Reseller and Grey channels. Value brands Moya and Karat win volume with ฿1,800–2,500 two-piece toilets (200–280 units each). The single highest-volume product is a Hafele ฿99 bidet spray (2,415 units) — a low-price accessory that drives traffic. Bubble size = monthly sales. source deck SKUs

| # | Brand | Category | Channel | Price ฿ | Units | Sales ฿K |

|---|---|---|---|---|---|---|

| 1 | Moya | Bathroom Fittings (toilet) | Reseller | 2,510 | 279 | 724 |

| 2 | Kohler | Showers & Faucets | Official | 10,511 | 46 | 526 |

| 3 | Cotto | Bathroom Fittings (toilet) | Official | 5,064 | 92 | 498 |

| 4 | Karat | Bathroom Fittings (toilet) | Reseller | 2,132 | 196 | 400 |

| 5 | Moya | Bathroom Fittings (toilet) | Reseller | 1,817 | 215 | 399 |

| 6 | Cotto | Bathroom Fittings (toilet) | Reseller | 4,750 | 68 | 323 |

| 7 | Cotto | Bathroom Fittings (toilet) | Official | 5,064 | 57 | 316 |

| 8 | Cotto | Bathroom Fittings (toilet) | Grey | 3,396 | 85 | 289 |

| 9 | Kohler | Showers & Faucets | Official | 2,260 | 123 | 275 |

| 10 | Cotto | Bathroom Fittings (toilet) | Grey | 597 | 399 | 247 |

Top 10 bestselling products, tracked set, April 2026. "Bathroom Fittings" here is predominantly toilets / two-piece sanitaryware (per product titles).

Kohler's bestsellers — premium showers, no toilets

Kohler holds a creditable 7 of the top 30 — but every one is a shower, faucet, hygiene spray or shower-filter refill, all sold through Official stores. Its hero is a ฿10,511 Aparu thermostatic shower column; volume comes from ฿700–2,300 hygiene sprays and the Exhale shower filter (which has a recurring refill SKU). Conspicuously absent: any toilet/sanitaryware product — the category's volume core, exactly where Cotto, Moya and Karat win. source deck SKUs

| Kohler product | Price ฿ | Units | Sales ฿K |

|---|---|---|---|

| Aparu 3-way thermostatic shower column | 10,511 | 46 | 526 |

| Watermind round handshower | 2,260 | 123 | 275 |

| Luxe hygiene spray (hose + bracket) | 1,133 | 190 | 221 |

| Luxe hygiene spray (Exclusive 1+1) | 2,090 | 90 | 188 |

| Exhale shower filter (set) | 2,290 | 77 | 176 |

| Exhale shower filter (refill) | 1,271 | 119 | 155 |

07 · Brand Differentiation

Channel, assortment & pricing

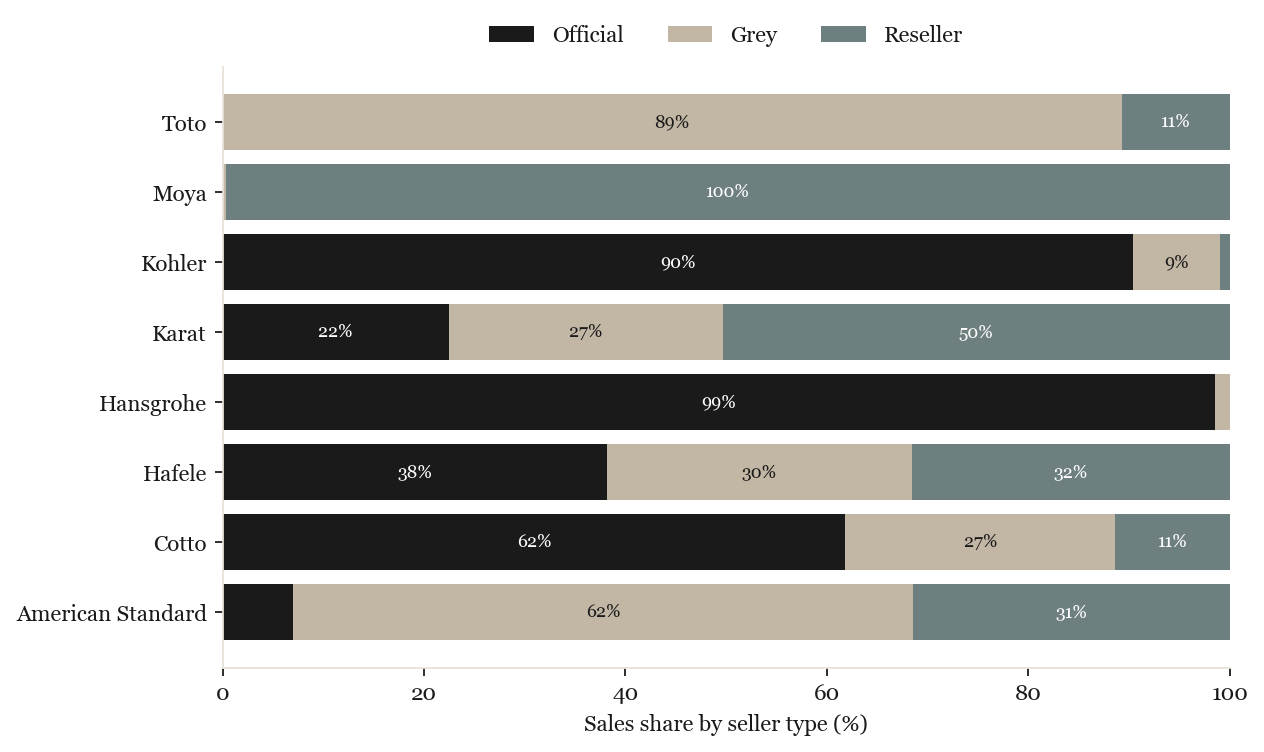

Channel — Kohler owns its storefront

90% of Kohler's sales flow through Official stores — the highest disciplined-channel share of any volume brand in the set (Cotto 62%, American Standard just 7%, Moya 100% reseller). This protects pricing and brand equity. source

Where Kohler plays — showers & faucets lead

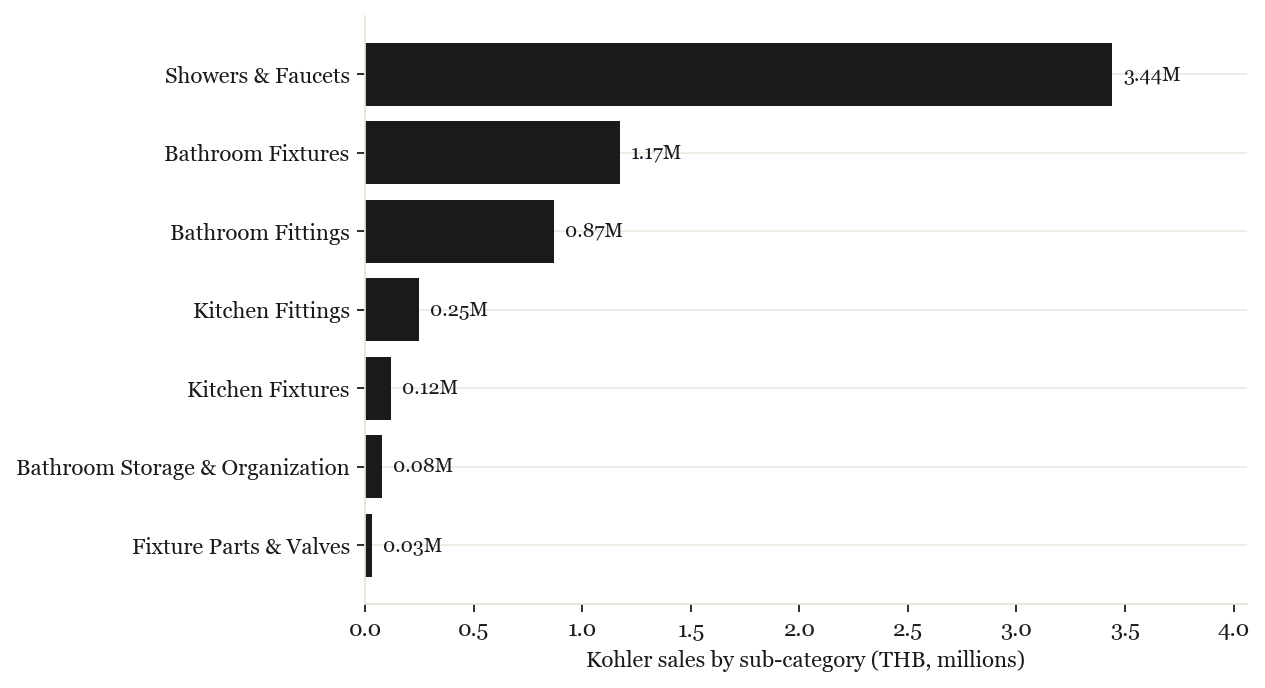

Kohler's Thai sales concentrate in Showers & Faucets (~58% of its sales), followed by Bathroom Fixtures and Fittings; kitchen lines are small. This is a focused, bathroom-led range rather than a broad home offer — a clear identity, but also a dependence on one product family. source

Assortment — narrow but efficient

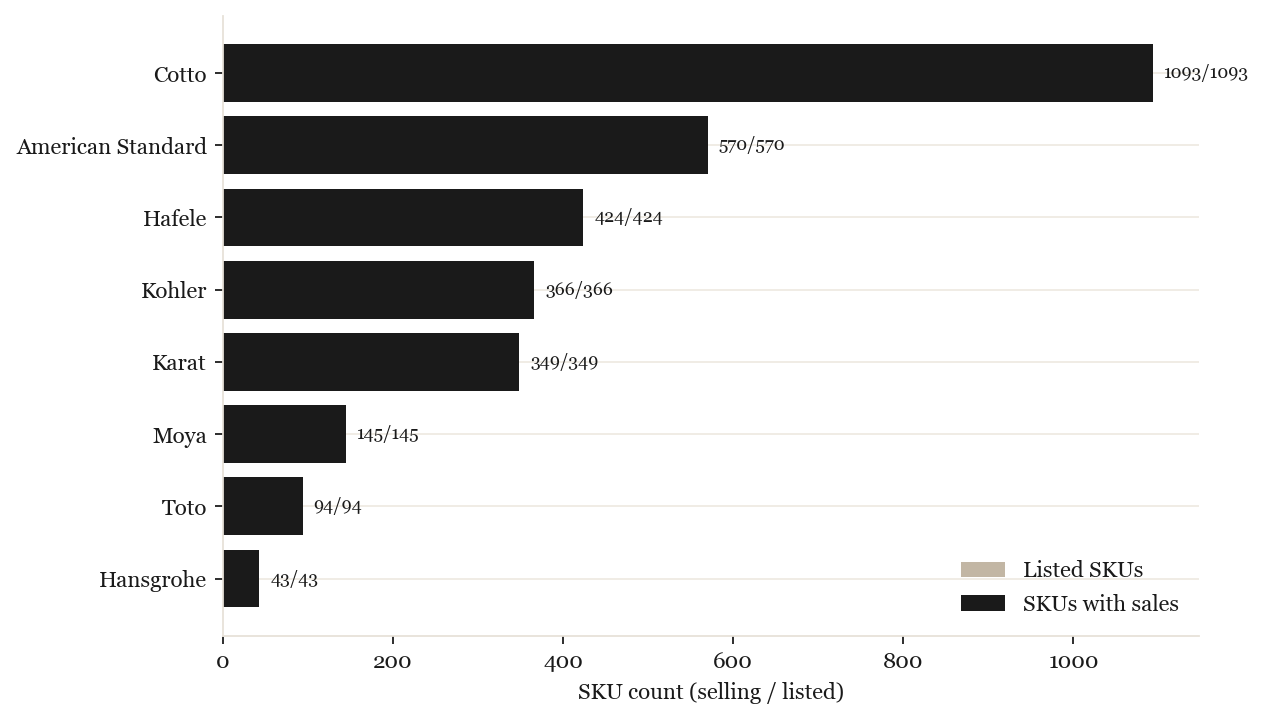

Kohler sells through 366 active SKUs and only 19 sellers — a far tighter footprint than Cotto (1,093 SKUs / 69 sellers) or American Standard (570 / 47). Fewer SKUs, more sales per listing: a focused, premium range rather than a long tail. source

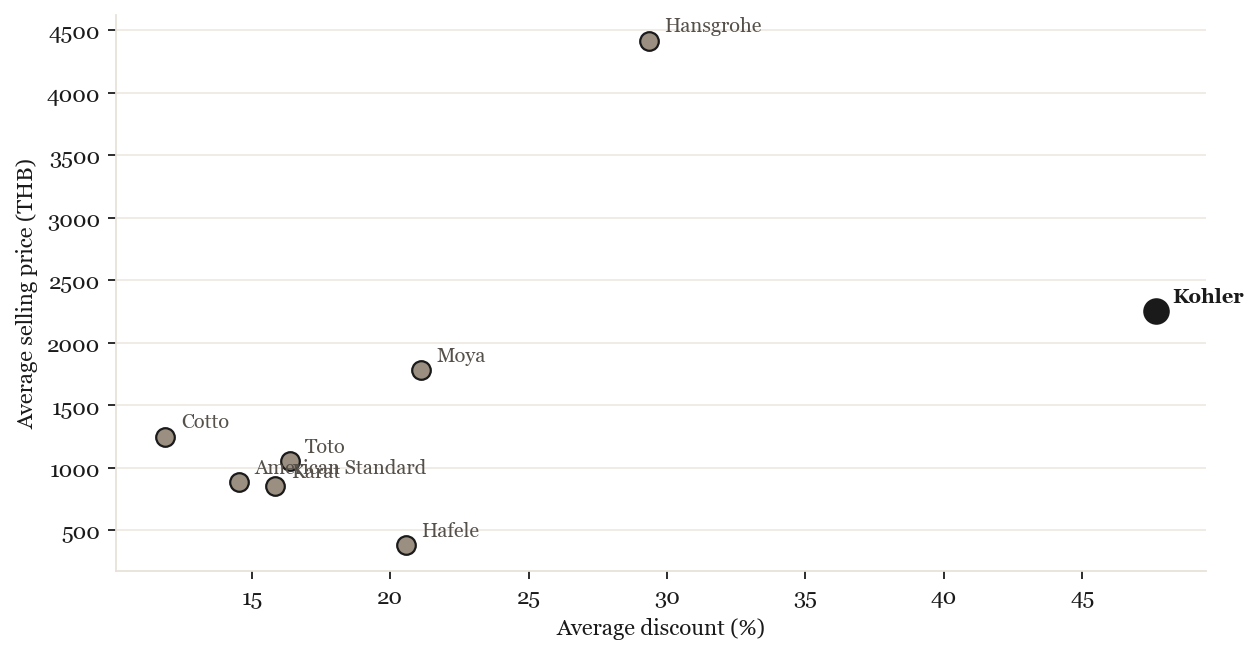

Pricing — premium, but heavily discounted

Kohler's ฿2,253 ASP is the second-highest in the set and 97% of its sales sit above ฿700 — clearly premium. The concern: a 48% average discount, the deepest of any brand (rivals 12–29%). Volume is being bought with price. source

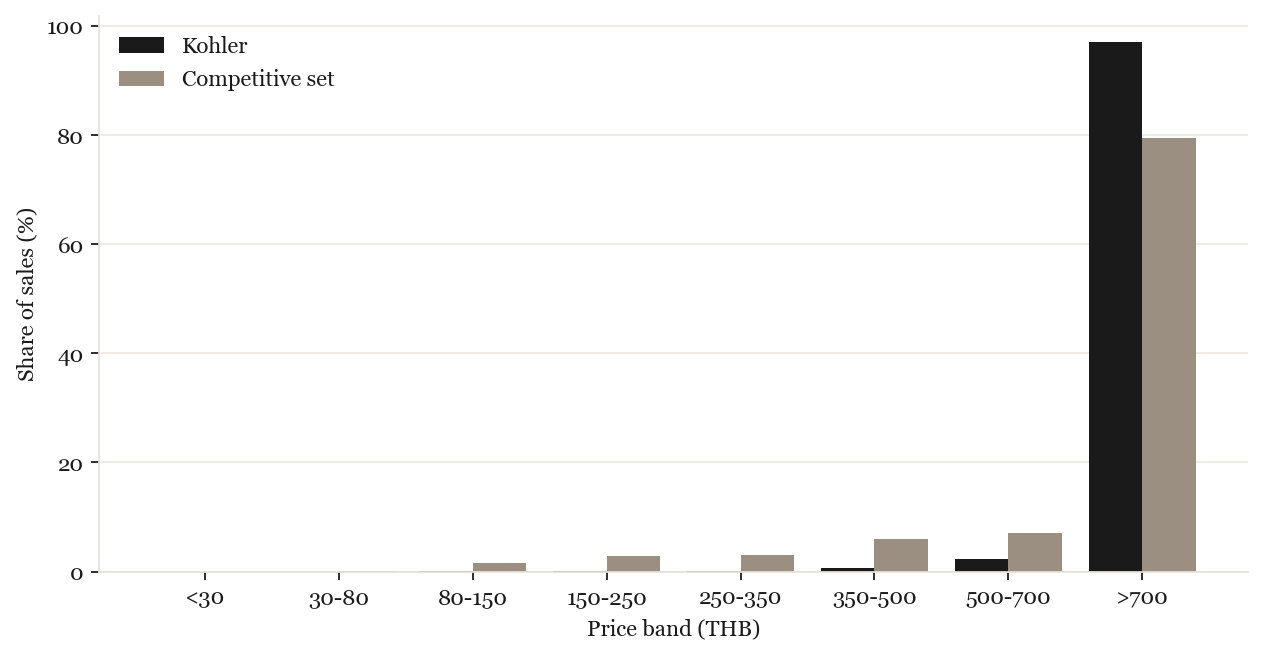

Pricing tier — the most top-heavy brand in the set

97% of Kohler's sales sit above ฿700 — even more concentrated than an already-premium set (79%). The ฿350–700 mid-premium tier, where competitors capture ~13% of demand, is barely addressed by Kohler (~3%). That protects positioning but cedes a growing middle to value brands. source

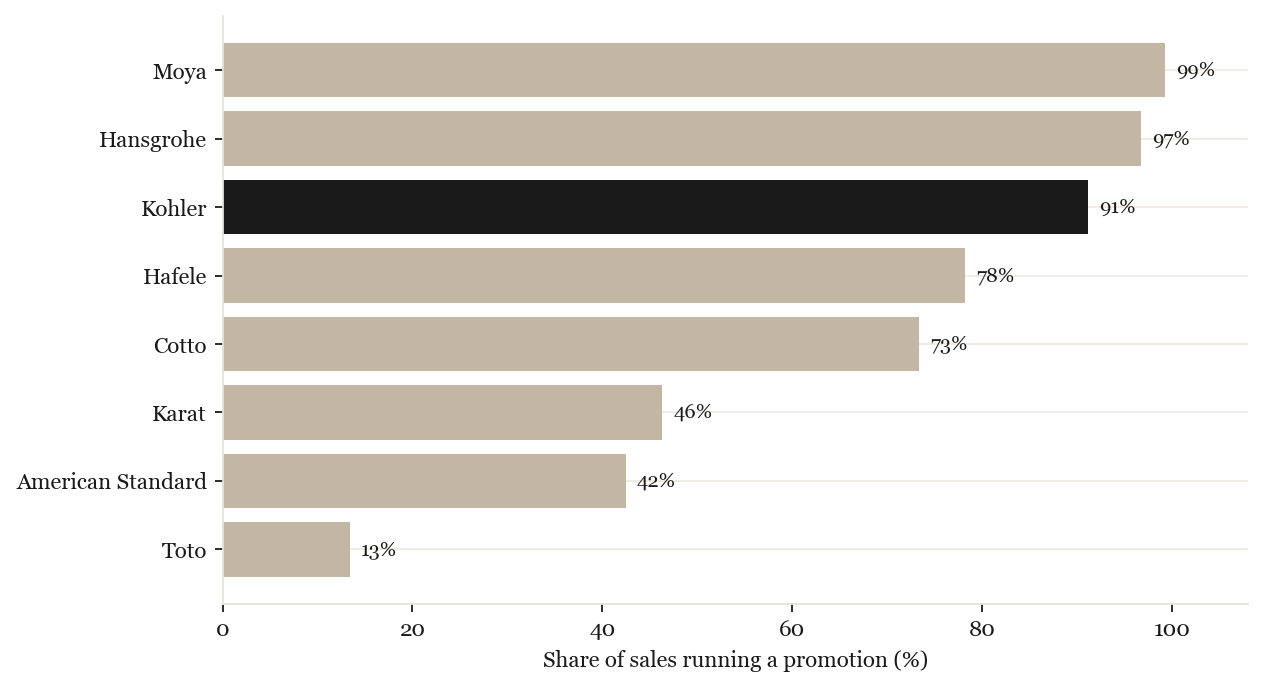

Promotion reliance — a flag on the discount strategy

91% of Kohler's sales run on a promotion — among the highest in the set (Moya 99%, Hansgrohe 97%) and far above disciplined players Toto (13%) and American Standard (42%). Combined with the 48% average discount, this is hard evidence that volume is being bought with price — the clearest margin and brand-equity watch-point in this review. source

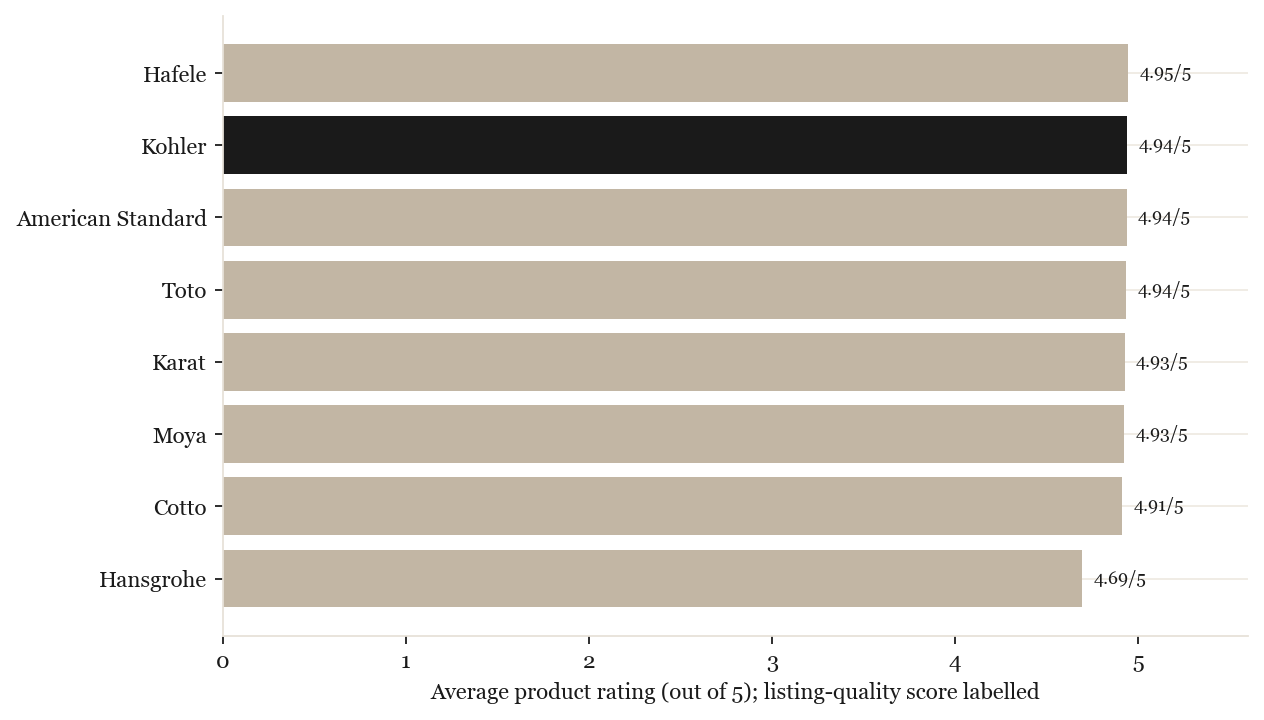

Listing quality — table stakes

Every brand clusters around 4.9/5 on product ratings, so listing quality is a baseline expectation rather than a point of difference. source

08 · Six-Month Outlook

Where the next two quarters point

Directional calls grounded in the 4-month trajectory and the deck's 13-month seasonality. Ranges are indicative, not forecasts — only ~13 months of history exist.

| Theme | Direction | Read |

|---|---|---|

| Category demand | ↑ (choppy) | Rebound likely from the April trough into mid-year; YoY trajectory strongly positive (+136% MAT). Expect seasonal swings, not a sustained decline. |

| Kohler set share | →/↑ | Hold-to-extend #2; plausibly ~18–24% of the set if Official-store strength and promotional support continue. Upside if it converts American Standard's lapsed premium buyers. |

| Competitive risk | watch | Value brands (Karat Faucet, Moya, Karat) gaining in mid-price tiers; any American Standard recovery would re-contest the premium. |

| Margin quality | watch | 48% discount dependence + 91% promo-on-sales is the key vulnerability — share held this way is fragile if promo intensity eases. |

Seasonality & long-horizon basis: EMI deck 13-month trend & MAT. source

External signals — forward-looking context

Surfaced by Aissistance Deep Research; treat as forward-looking signals rather than already-realised changes in our April data.

| Signal | Type | Read & implication for Kohler |

|---|---|---|

| Building Energy Code & TISI water-saving standards | tailwind | Regulatory push for water-efficient fixtures pulls the category up-market. Premium-positioned brands benefit; emphasise water-saving credentials in PDP & marketing. EXT ↗ |

| Aging-in-place demographic shift | tailwind | Affluent over-65s drive demand for universal-design bathrooms (grab bars, walk-in showers, smart-bidet retrofits). JOMOO already has a "Senior Suite" range — Kohler should productise an accessibility tier. EXT ↗ |

| SCG Decor × Hansgrohe / AXOR alliance | critical risk (forward) | Reported 42–53% discount offensive on Shopee/Lazada premium fixtures via this partnership. Our April data still shows Hansgrohe small (~1.4% set share) — this is a ramping signal, not realised share. Monitor monthly. EXT ↗ |

| Marketplace fulfilment / installation friction | structural ceiling | Shopee/Lazada logistics Trustpilot 1.4★, ~75% cart abandonment in home-improvement, severe Pantip-documented installation failures. Limits how far a pure-e-commerce strategy can go for heavy fixtures; productising installation (Action #9) directly addresses this. EXT ↗ EXT ↗ |

09 · AI Action Plan

Nine moves — refined and extended by external research

The marketplace data drove six initial moves; an external Aissistance Deep Research pass refined

three of them, surfaced three new fronts, and reframed the toilet recommendation. Internal-evidence moves are

grey-pilled; research-influenced moves carry a blue EXT ↗ tag and link to the cited source.

1 · Capture AmStd's vacated premium

Conquest-target the premium demand American Standard is leaving behind (LIXIL is shifting Grohe/INAX to offline LIXIL Experience Centres). EXT ↗2 · Fortify the Official-store moat

Defend channel with exclusive SKUs and complex bundles that resellers can't price-match — the SCG × Hansgrohe assault is the catalyst. EXT ↗3 · Migrate to GWP-led promotion

Replace blanket 48% discounts with Gift-With-Purchase mechanics (Dyson playbook) — platforms algorithmically penalise promo-quiet brands. EXT ↗ EXT ↗4 · Open the ฿350–700 mid-premium tier

97% of Kohler sales sit above ฿700; mid-premium products widen the funnel against rising value brands.5 · Shopee depth, Lazada selective

Defend ~88% Shopee leadership; treat Lazada as a curated premium boutique, not a broad push.6 · Contest smart toilets, not ceramic

Cotto's mass-toilet moat is structurally fortified by SCG's vertical integration — attack at the smart-toilet & retrofit-bidet level instead. EXT ↗7 · Retrofit Bidet conquest

Target Cotto's installed base with premium electronic bidet seats that fit existing standard toilets (12% CAGR sub-segment). EXT ↗8 · Filter Lifecycle remarketing

Automated retargeting timed to shower-filter end-of-life on Shopee, Lazada and Line — recurring models deliver 3–5× LTV.9 · Productise installation

Bypass marketplace fulfilment failure (Shopee/Lazada Trustpilot 1.4★) with a Kohler-certified white-glove install service — the "Installation Moat". EXT ↗ EXT ↗Detail & rationale

- Capture American Standard's vacated premium demand. AmStd's −82% online collapse looks structural — LIXIL is reallocating Grohe/INAX behind offline LIXIL Experience Centres in Bangkok, conceding marketplace share. Target lapsed AmStd buyers with Official-store assurance, warranty depth and bundles. source EXT ↗ LIXIL pivot

- Fortify the Official-store moat with SKU exclusivity, not price. The 90% Official-store share is Kohler's structural edge. Defend it from the SCG-backed Hansgrohe assault (44–53% off vouchers on Shopee/Lazada) with exclusive online-only SKUs and complex bundle sets resellers can't price-match — not by engaging in a race to the bottom. source EXT ↗ partnership

- Migrate from blanket discounting to GWP-led promotion. 91% of Kohler's sales already run on promotion at an average 48% discount. Total cessation isn't viable — Shopee/Lazada algorithmically penalise promo-quiet brands — but Kohler can adopt the Dyson Thailand playbook: free premium filters, extended warranties, exclusive accessories as Gift-With-Purchase, preserving ASP while satisfying platform mechanics. source EXT ↗ EXT ↗

- Open the ฿350–700 mid-premium tier. 97% of Kohler's sales sit above ฿700 versus 79% for the set — Kohler is the most top-heavy brand. A deliberate mid-premium range (or accessory/bundle entry points) widens the funnel against value brands gaining there. source

- Press the Shopee advantage; build Lazada selectively. ~88% of branded category sales run through Shopee — defend it hard. Treat Lazada (~19% of set sales) as a curated premium boutique for high-ticket smart fixtures, not a broad push. source

- Reframe the toilet play: cede ceramic mass, contest smart toilets & retrofit bidets. Cotto's volume-toilet dominance is structurally fortified by SCG's ฿25bn-revenue vertical integration and "ECO COTTO" branding — a volume war is unwinnable. Compete instead in the high-margin smart toilet and retrofit electronic bidet seat tiers, where Kohler's premium positioning and showers/sprays expertise transfer naturally. source EXT ↗

- Launch a Retrofit Bidet conquest campaign targeting Cotto owners. The retrofit smart-bidet-seat sub-segment is growing at ~12% CAGR and addresses condo-living constraints (no plumbing change). Marketing a ~฿15k retrofit bidet as a hygiene/wellness upgrade is far more viable than pushing a full bathroom renovation in a market where 66% of consumers report cutting spending — and it monetises Cotto's installed base instead of trying to displace it. EXT ↗

- Build a Filter Lifecycle remarketing engine. The Exhale shower filter and its refill SKU are already Kohler bestsellers — a recurring revenue loop bringing customers back several times a year. Instrument average filter lifespan, then deploy automated lifecycle-timed remarketing across Shopee, Lazada and Line. Consumable-replenishment models deliver 3–5× LTV uplift in adjacent premium categories. source

- Productise white-glove installation — the "Installation Moat". Thai consumer-forum evidence (Pantip) catalogues disastrous third-party installs of heavy fixtures (cracked pipes, flooding); marketplace fulfilment scores Trustpilot 1.4–1.5★. SCG's Q-CHANG and HomePro's vFIX are pivoting the market from selling products to "Home as a Service". A Kohler-certified install fleet (own or partnered) bundled with smart-toilet and retrofit-bidet purchases would convert anxiety into conversion — and is harder to replicate than any SKU advantage. EXT ↗ EXT ↗

10 · Sources

Every insight, traced

Click any insight's “source” tag above, or any thumbnail below, to view the underlying slide or chart. Derived charts are computed from EMI × Kohler TH SKU-level data (Jan–Apr 2026, Lazada + Shopee); deck pages are from the EMI × Kohler TH April 2026 report.

External research

Aissistance Deep Research, 3-pass run (June 2026). Each item below links out to the cited source in a new tab.